Insurance products have very high sales commissions, which is why we at New Perspectives try to discourage clients from buying them. Generally, most benefits of an annuity are replicable in a carefully managed investment account for much lower fees, therefore more potential for return.

Because the sales commissions are so high, the sales people push these products hard. Many people know of a friend or family member who was pushed into an expensive contract that they didn't totally understand. The hard sell tactics toe a fine line between salesmanship and fraud. Just like during the mortgage and housing boom when incentives to make mortgages led to hard sells, deception and sometimes outright fraud, insurance sales people can push into murky territory easily.

According to this article, Florida is doing something about that. High suitability requirements are being extended to people of all ages (we don't think annuities are suitable for just about anybody!). The laws also extend the amount of time people have to decide about their purchase and restrict the surrender periods.

Surrender periods are one of the worst features of annuities. Annuities tie up your money, but surrender charges make it expensive to untie your money. Typically these are in a schedule of declining fees over 7-12 years. It is possible to get annuities from Vanguard of Jefferson National with excellent investment options and no surrender charges - so keep that in mind when someone says that theirs is the best. Talk with a fee only, fiduciary advisor for advice that is in your best interest.

Independent, Fee-Only Financial Advisor

Wednesday, March 13, 2013

Tuesday, March 05, 2013

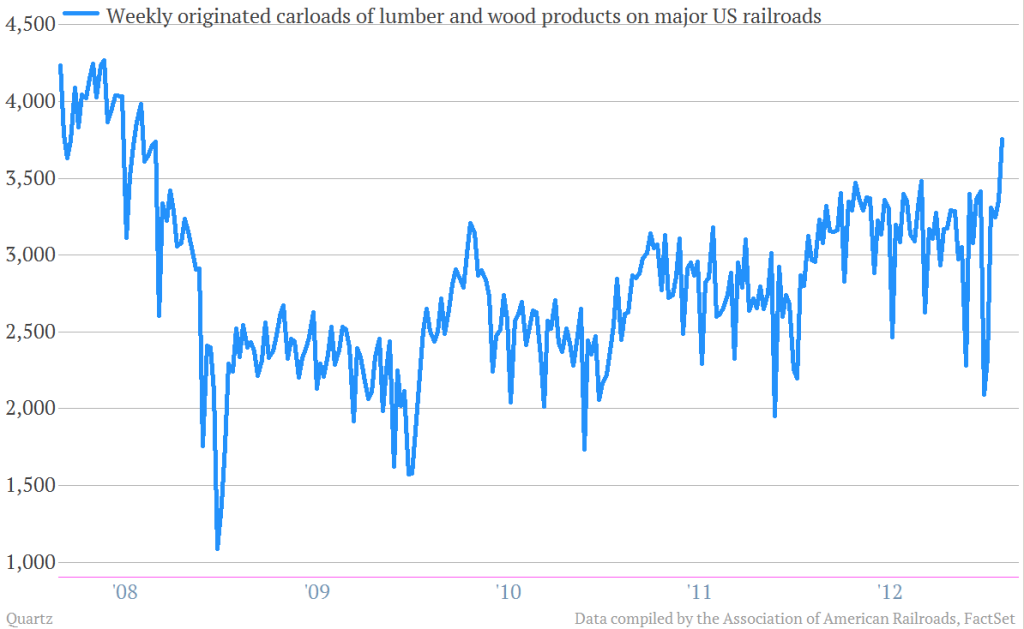

Housing Recovery

One interesting indicator behind housing is Lumber. Lumber is, of course, used to build houses in America, and is a key ingredient in many home improvement projects (like the shelves I just built in my closet this weekend).

The price of lumber is dictated by supply and demand, of course, and that has been a rising price lately. For much of the past 5 years, lumber prices have been between $150 and $250, with two peaks above $300. The end of 2012 and the first two months of this year have seen those prices hit close to $400.

The price of lumber is dictated by supply and demand, of course, and that has been a rising price lately. For much of the past 5 years, lumber prices have been between $150 and $250, with two peaks above $300. The end of 2012 and the first two months of this year have seen those prices hit close to $400.

Looking at charts in this article, lumber shipments appear to follow a seasonal pattern reflected in housing prices. This time looks to be different. The seasonal decline in lumber shipments has not been as large as usual. Combining rising lumber prices with greater shipments means much more money is being spent on lumber now than at the peak. When money flows representing desires and expectations in the economy, more money going to lumber means more confidence in housing - a huge driver of the American economy.

Subscribe to:

Comments (Atom)